Esteemed Wall Street media analyst Michael Nathanson on Monday released an investor note that, for the most part, asks Fox Corporation C-Suiters to take a long, hard look at its networks and owned-and-operated stations and perhaps put them up for sale.

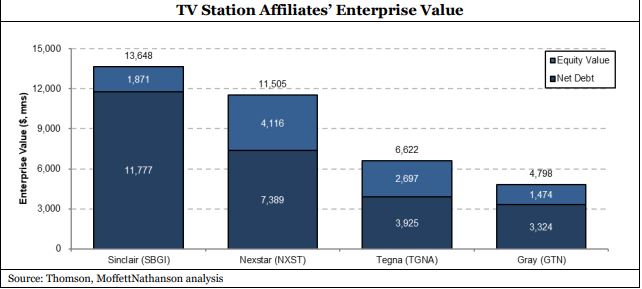

In doing so, Nathanson offered some perspective on the enterprise value of four “major pure-play station operators.” They range from $4.8 billion to $13.6 billion.

The enterprise value he pegs for the FOX network and O&Os at $10.93 billion.

It’s great news for Gray Television. But, Nathanson’s baffled. “That makes no sense,” he says.

BE SURE TO ‘LIKE’ RBR+TVBR ON FACEBOOK!

Nathanson took a magnifying glass to Sinclair Broadcast Group, Nexstar Media Group, TEGNA and Gray, just to compare their value to that of FOX’s owned stations and its broadcast network.

“While these station operators are not burdened with the operation of a national network’s prime-time programming slate, there is value in Fox’s O&O station footprint, which generates the majority of the EBITDA for the company’s television segment, that is not currently priced into the stock,” Nathanson says.

What does this signify? “The market is effectively saying that Gray TV is worth more than the FOX network and the Fox O&O stations. That makes no sense.”

Why? “Given the high losses generated by sports contracts at the national network level and the high margins of Fox’s non-O&O affiliates, it would be logical to assume that these unaffiliated stations have to continue to kick in higher and higher reverse retrans rates going forward.”

Moreover, Nathanson finds that Sinclair, Nexstar, TEGNA and Gray have historically traded around 7.5x. “At the 7.0x multiple we currently ascribe to Fox’s Cable Networks, [with other conditions remaining the same], Fox’s Television segment (ex-Tubi) would be awarded a -17.8x multiple by the market,” Nathanson concludes. “Even if Fox Television doesn’t reach the 7.5x historical average multiple of the major station operators, there

is a clear disconnect between Fox’s current stock price and the underlying value of its assets.”

While the evaluation is certainly good for Gray, it comes in the context of a blistering assessment of what Fox executives should do regarding its broadcast network, which came of age some 30 years ago, and its owned-and-operated stations — including WTTG-5 in Washington, D.C.; WNYW-5 in New York; WFLD-32 in Chicago; KTTV-11 in Los Angeles; and WOFL-35 in Orlando.

“We see untapped value at the FOX network for TV studio owners like WarnerMedia or cable network operators like Discovery and WarnerMedia or any entity looking to use the power of broadcast to launch new Direct-to-Consumer scripted content platforms,” Nathanson says. “We would urge Fox management to renew their Sunday NFL package, pass on the loss-making Thursday NFL package, and use the two-year anniversary of their life as a new company in March 2021 to consider their options vis-à-vis the television assets.”