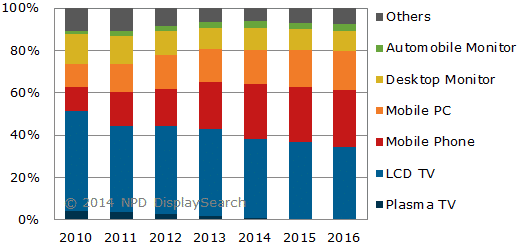

Since 2006, LCD TV has accounted for the largest share of flat panel display (FPD) revenues; however, in 2014, mobile displays will take the lead. According to the latest NPD DisplaySearch Quarterly Worldwide FPD Shipment and Forecast Report, combined FPD revenues from mobile PCs and mobile phones will comprise 42% of total global FPD revenues in 2014, for the first time surpassing LCD TV at 37%.

Since 2006, LCD TV has accounted for the largest share of flat panel display (FPD) revenues; however, in 2014, mobile displays will take the lead. According to the latest NPD DisplaySearch Quarterly Worldwide FPD Shipment and Forecast Report, combined FPD revenues from mobile PCs and mobile phones will comprise 42% of total global FPD revenues in 2014, for the first time surpassing LCD TV at 37%.

Due to their larger display area and comparatively higher unit prices, LCD TV panels accounted for a majority of FPD revenues since 2006, but over the past three years, the market for mobile devices has expanded. The recent trend toward higher resolutions, slimmer and more lightweight specifications, wider view angle requirements, lower power consumption, and the emergence of LTPS and OLED displays are causing mobile display revenues to soar.

“With strong growth in tablet PCs, high-end notebooks, and smartphones — especially high resolution and wide-viewing angle displays — mobile devices are leading the growth of the FPD industry,” said David Hsieh, vice president of NPD DisplaySearch. “Mobile devices are expected to expand their revenue lead over LCD TV in the years to come, accounting for nearly half of all FPD revenue by 2016.

Worldwide FPD revenues are expected to reach $131 billion in 2014, which is just 1% higher than the previous year. While mobile phones, mobile PCs, automobile monitors, public displays, and OLED TVs grow, display revenues for LCD TVs, plasma TVs, digital still cameras, and amusement devices will decline. The decline in LCD TV revenue is especially sharp, due to price erosion of 40-inch and larger panel sizes. LCD TV panel revenues are expected to fall from $53 billion in 2013 to $49 billion in 2014. At the same time, mobile PC display revenues are expected to climb from $20.3 billion to $21.2 billion in 2014 and mobile phone displays from $28.9 billion to $33.6 billion.

“The FPD industry is becoming increasingly dominated by smart handheld applications,” Hsieh noted. “The supply chain needs to leverage the mobile display boom, strategically deploying their resources, and developing new technologies.”

Because of the shift in the market toward mobile devices, FPD makers are now turning their focus to small and medium displays. This situation is especially apparent in China, where there are growing numbers of new LTPS and OLED fabs. On the other hand, panel makers in China are starting to use Gen 8 and other larger fabs to produce greater numbers of panels for small and medium-sized handheld devices.

“While Chinese panel manufacturers are comparatively slower and weaker than others when it comes to mobile panel technologies, they will definitely change their focus from LCD TV to the mobile displays,” Hsieh said.